For a more general overview of Opportunity Zones, please read my February 2019 blog post, “Everything You Need to Know About ‘Opportunity Zones.’”

In summary, new or expanding businesses located in an Opportunity Zone can potentially enjoy the following two tax benefits: a) Deferral of gain on new investments in such business until December 31, 2026; and b) Avoidance of gain after holding such assets for ten (10) years. In addition, an investor will receive a step-up in basis of 10% of the investment after holding the investment for five (5) years and an additional 5% step-up after seven (7) years.

I am a developer. How does the incentive help me fund projects in an Opportunity Zone?

The Opportunity Zone Tax Incentive can lower the cost of equity for expanding or improving businesses located inside an opportunity zone. The deferral portion of the incentive lowers the cost of equity by about 400 basis points, while the avoidance portion is a function of the exit price after the ten (10) year hold.

Project developers that can place qualified equity (“OZ Equity”) can, generally, reduce their cost of equity by at least 400 basis points.

Here is how that reduction looks in the commercial real estate context. A typical commercial real estate development with a credit worthy tenant might command a return on equity of 10% and require equity for 35% of the project’s cost. At a debt rate of 5%, the project would have a weighted cost of capital of 7.25%. If the OZ Equity will take a return of 6% and comprise 20% of the equity stack, the weighted cost of equity drops to 6.45%.

What are the legal concerns of raising Opportunity Zone equity?

Limited partnership and LLC interests are generally presumed to be securities, and therefore subject to the Securities Act of 1933 and applicable state regulation due to classification as investment contracts.

Montana has taken a broad view as to what constitutes an investment contract, going so far as to classify certain tenant-in-common interests as a “security” subject to regulation.

Promoters and developers may also be subject to registration as investment companies or classification as investment advisors.

What role does Site Control play?

The unique geographic parameters of the incentive place a premium on-site availability and selection. Developers should consider a number of strategies to enhance site viability and availability. Here are a few considerations and strategies:

- Use of long-term ground leases to lower land acquisition costs or to address related party issues with acquisition.

- Pooling arrangements with adjacent property owners to increase project size.

- Option Agreements.

- Managing price inflation.

Site control will generally be the first step in a project pipeline and critically should come before any OZ Equity is placed.

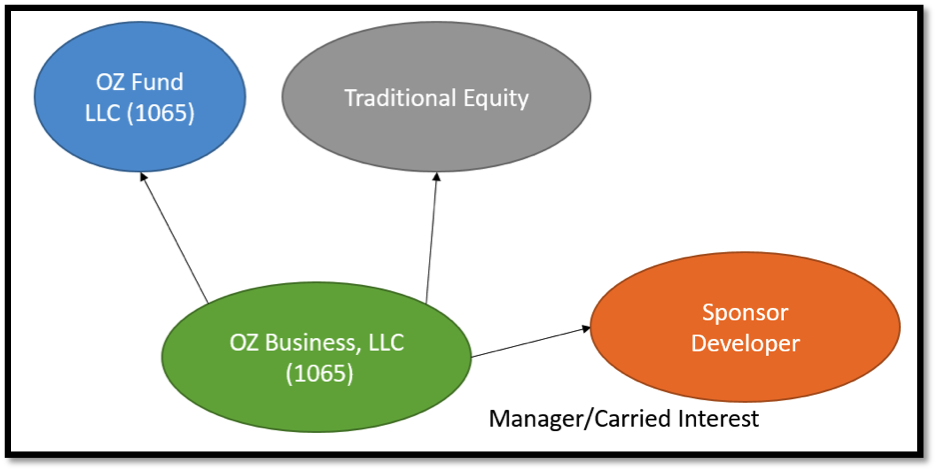

How will the incentive work in a typical project?

- Allows for the OZ Fund to be raised organically or for an existing OZ Fund to acquire an interest.

- OZ Fund can potentially “swap” in and out of OZ business.

- Developer/Sponsor retains control of development.

Allows for traditional equity. Traditional equity has value given the zero capital accounts of the OZ equity.

How long is the incentive applicable?

Of the three tax incentives offered by the OZ incentive, only the deferral incentive is perishable in the near-term. Applicable deferred gain must be recognized on December 31, 2026. So, the longer an investor waits to invest, the smaller the avoidance period.

An investor that acquires an Opportunity Fund interest after December 30, 2019, will not be able to apply the 5% basis step-up to their avoided gain. However, pursuant to the Second Tranche of proposed regulations, if the Opportunity Fund is a partnership (and presumably also an S Corporation) this step-up will be available to the taxpayer to offset items of income, loss, deduction, or credit which are distributed to the owner of the interest in a qualified Opportunity Fund.

What types of businesses qualify for the incentive despite conducting activity outside of a Zone?

The Second Tranche of Regulations proposes three independent safe harbors for when an operating business that conducts activity/commerce that is in part outside of a zone will qualify as an Opportunity Zone Business. Here are those tests:

- 50% of services as measured in hours performed by independent contractors and employees for the Opportunity Zone Business must occur within the Zone.

- 50% of compensation for services performed by independent contractors and employees for the Opportunity Zone Business must be made with respect to activity within the Zone.

50% of the Opportunity Zone Business’s gross income must be derived from tangible property located in the opportunity zone and “management and operational” functions of the business within the zone.

Worden Thane P.C. has a strong Business and Tax Law practice. Please feel free to contact Ross P. Keogh for advice on Opportunity Zones and how to benefit from them.